Are You Defining Items in QuickBooks Correctly?

")

[vc_row][vc_column][vc_column_text]

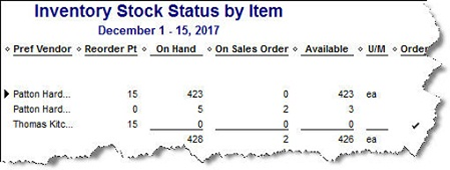

Create item records in QuickBooks carefully, and QuickBooks will return the favor by running useful, accurate reports.

Figure 1: Clearly-defined items result in precise reports.

Obviously, you’re using QuickBooks because you buy and/or sell products and/or services. You want to know at least weekly — if not daily — what’s selling and what’s not, so you can make informed plans about your company’s future.

You get that information from the reports that you so painstakingly customize and create. But their accuracy depends in large part on how carefully you define each item. This can be a laborious process, but it’s a critical part of QuickBooks’ foundation.

QuickBooks’ Item Lineup

You may not be aware of all of your options here. So let’s take a look at what you see when you go to Lists | Item List | Item | New:

Service. Simple enough. Do you or your employees do something for clients? Training? Construction labor? Web design? This is usually tracked by the hour.

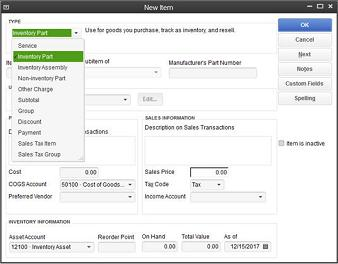

Inventory Part. If you want to maintain detailed records about inventory that contain up-to-date information about the value, quantities on hand and cost of goods sold, you must define these items as inventory parts. Before you start creating individual records, make sure that QuickBooks is set up for this purpose. Go to Edit | Preferences | Items & Inventory | Company Preferences and select the desired options there, like this:

Figure 2: QuickBooks needs to know that you’re planning to track at least some items as inventory parts.

Inventory Assembly. Just what it sounds like; it’s sometimes referred to as a Bill of Materials. Do you sell items that actually consist of multiple individual products, services and/or other charges (though you may also sell the parts separately)? If you’re planning to track the compilations as individual units, then you must define them as assemblies.

Non-Inventory Parts. If you don’t track inventory, you can set up items as non-inventory parts. Even if you do track inventory, there may be times when you’ll want to use this designation. For instance, you might sell something to a customer that they asked you to obtain, but you don’t plan to stock it. In that case, QuickBooks only records the incoming and outgoing funds.

Figure 3: The New Item window looks a bit intimidating, but it’s critical that you complete it thoroughly and correctly. We can help you get started.

Other Charges. This is a catch-all category for items like delivery charges or setup fees. You can’t designate a unit or measure here; they’re just standard costs.

Groups. Unlike assemblies, these are not recorded as individual inventory units. Use this designation when you sell a combination of items together frequently but you don’t want them tracked as one entity.

Discount. This is a fixed amount or a percentage that you subtract from a subtotal or total.

Payment. Normally, you would use the Receive Payments window to record a payment made. But if your customer has made a partial or advance payment upfront, use this item to subtract it from the total when you create the invoice or statement.

Figure 4: Use the Payment item to record an upfront remittance.

Sales Tax Item. One sales tax, one rate, one agency. Sales Tax Group. If a sale requires two or more sales tax items, QuickBooks calculates the total and displays it for the customer, but the items are tracked individually.

Additional Actions

The Item menu provides other options for working with items. You can:

- Edit or delete

- Duplicate

- Make inactive

- Find in transactions and

- Customize the list’s columns.

Let us know if you’re not confident about items you’ve already created or if you’re just getting started with this important QuickBooks feature. Some extra work and attention upfront can save you from hours of back-tracking and frustration – and from reports that don’t tell the truth.

[/vc_column_text][/vc_column][/vc_row]

College Funding: Investing Versus Borrowing

College Funding: Investing Versus Borrowing If something is worth $1, would you rather pay $1.46 for it, or would you prefer a price of $0.66? That, in a nutshell, is a choice that families must make as they prepare to pay for the cost of college education for their children. Saving and investing for college…

What Real Estate Investors Need To Know About Property Management

What Real Estate Investors Need To Know About Property Management By James Kobzeff Once you purchase a real estate rental property, you virtually become the CEO of your own small business. Sure, you feel good about becoming a landlord and owner of your own private money-maker, but unless it’s raw land, your work has just…

Rent Vs. Buy Your First Home

Rent vs. Buy Your First Home Should you rent or should you buy your home? It takes more than looking at your mortgage payment to answer this question. This calculator helps you weed through the fees, taxes, and monthly payments to help you make a good financial decision. Click the “View Report” button for a…

IRS Announces 2015 Standard Mileage Rates

IRS Announces 2015 Standard Mileage Rates By Alan Olsen, CPA, MBA (tax) Managing Partner Greenstein Rogoff Olsen & Co. LLP Although most people typically use their vehicles to commute back and forth to work, there are many individuals that are required to use their personal vehicles as part of their job. Did you know that…