Sale of Residence – Real Estate Tax Tips

[vc_row][vc_column][vc_column_text]

Sale of Residence – Real Estate Tax Tips

You may qualify to exclude from your income all or part of any gain from the sale of your main home. Your main home is the one in which you live most of the time.

Ownership and Use Tests

To claim the exclusion, you must meet the ownership and use tests. This means that during the 5-year period ending on the date of the sale, you must have:

- Owned the home for at least two years (the ownership test)

- Lived in the home as your main home for at least two years (the use test)

Gain

If you have a gain from the sale of your main home, you may be able to exclude up to $250,000 of the gain from your income ($500,000 on a joint return in most cases).

- If you can exclude all of the gain, you do not need to report the sale on your tax return

- If you have gain that cannot be excluded, it is taxable. Report it on Schedule D (Form 1040)

Loss

You cannot deduct a loss from the sale of your main home.

Worksheets

Worksheets are included in Publication 523, Selling Your Home, to help you figure the:

- Adjusted basis of the home you sold

- Gain (or loss) on the sale

- Gain that you can exclude

Reporting the Sale

Do not report the sale of your main home on your tax return unless you have a gain and at least part of it is taxable. Report any taxable gain on Schedule D (Form 1040).

More Than One Home

If you have more than one home, you can exclude gain only from the sale of your main home. You must pay tax on the gain from selling any other home. If you have two homes and live in both of them, your main home is ordinarily the one you live in most of the time.

Example One:

You own and live in a house in the city. You also own a beach house, which you use during the summer months. The house in the city is your main home; the beach house is not.

Example Two:

You own a house, but you live in another house that you rent. The rented house is your main home.

Business Use or Rental of Home

You may be able to exclude your gain from the sale of a home that you have used for business or to produce rental income. But you must meet the ownership and use tests.

Example:

On May 30, 1997, Amy bought a house. She moved in on that date and lived in it until May 31, 1999, when she moved out of the house and put it up for rent. The house was rented from June 1, 1999, to March 31, 2001. Amy moved back into the house on April 1, 2001, and lived there until she sold it on January 31, 2003. During the 5-year period ending on the date of the sale (February 1, 1998 – January 31, 2003), Amy owned and lived in the house for more than 2 years as shown in the table below.

| Five Year Period | Used as Home | Used as Rental |

|---|---|---|

|

2/1/98-5/31/99 |

16 months |

|

|

6/1/99-3/31/01 |

22 months |

|

|

4/1/01-1/31/03 |

22 months |

|

|

38 months |

22 months |

Amy can exclude gain up to $250,000. However, she cannot exclude the part of the gain equal to the depreciation she claimed for renting the house.[/vc_column_text][/vc_column][/vc_row]

Reducing Risk With a Diversified Portfolio

Reducing Risk With a Diversified Portfolio Have you been worried about the stock market’s recent volatility? You’re not alone. The stock market in March was a roller-coaster ride that served as a reminder to investors that the market’s ups and downs can be a little dizzying. But a volatile market should not leave you feeling…

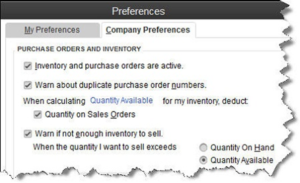

Are You Defining Items in QuickBooks Correctly?

[vc_row][vc_column][vc_column_text] Create item records in QuickBooks carefully, and QuickBooks will return the favor by running useful, accurate reports. Figure 1: Clearly-defined items result in precise reports. Obviously, you’re using QuickBooks because you buy and/or sell products and/or services. You want to know at least weekly — if not daily — what’s selling and what’s…

Saving Money for College: Education Credits

Saving Money for College: Education Credits Education credits are tax credits available for qualified education expenses paid by the taxpayer in the furthering of their education. Qualified education expenses are defined as an expense paid during the tax year for tuition and fees required by an eligible educational institution for student enrollment and attendance. Room…

Thinking About Giving up Your U.S. Citizenship? Think Twice

Thinking About Giving up Your U.S. Citizenship? Think Twice While not a lot of people ever entertain the thought of giving up their U.S. citizenship, there are more people every year that are making that choice. Among them are several wealthier people whose main reason for renouncing is to escape the country’s overloaded tax system;…