Sales Tax Deduction Option, State and Local

[vc_row][vc_column][vc_column_text]

Sales Tax Deduction Option, State and Local

The Tax Relief and Health Care Act of 2006 extended the election to deduct state and local general sales taxes for 2006. The act was enacted after Schedule A (Form 1040), Itemized Deductions, and its instructions were printed. Because we were not able to include the instructions for figuring the deduction in the Schedule A instructions, we are providing this publication to help you figure this deduction.

You can elect to deduct state and local general sales taxes instead of state and local income taxes as a deduction on Schedule A. You cannot deduct both. To figure your deduction, you can use either:

- Your actual expenses, or

- The optional sales tax tables plus the general sales taxes paid on certain specified items.

IRS Publication 600, Optional State Sales Tax Tables, helps taxpayers determine their sales tax deduction amount in lieu of saving their receipts throughout the year. Taxpayers use their income level and number of exemptions to find the sales tax amount for their state. The table instructions explain how to add an amount for local sales taxes if appropriate.

Taxpayers also may add to the table amount any sales taxes paid on:

- A motor vehicle, but only up to the amount of tax paid at the general sales tax rate; and

- An aircraft, boat, home (including mobile or prefabricated), or home building materials, if the tax rate is the same as the general sales tax rate.

For example, the State of Washington has a motor vehicle sales tax of 0.3 percent in addition to the state and local sales tax. A Washington state resident who purchased a new car could add the tax paid at the general sales tax rate to the table amount, but not the 0.3 percent motor vehicle sales tax paid.

Taxpayers will claim the deduction on line 5 of Schedule A, checking a box to indicate whether the amount represents sales tax or income tax.

While this deduction will mainly benefit taxpayers with a state or local sales tax but no income tax — in Alaska, Florida, Nevada, South Dakota, Texas, Washington and Wyoming — it may give a larger deduction to any taxpayer who paid more in sales taxes than income taxes. For example, you may have bought a new car, boosting your sales tax total, or claimed tax credits, lowering your state income tax.[/vc_column_text][/vc_column][/vc_row]

Making Tax-wise Investments

Making Tax-wise Investments Tax considerations are not, and should never be, the be-all and end-all of investment decisions. The choice of assets in which to invest, and the way in which you apportion your portfolio among them, almost certainly will prove to be far more important to your ultimate results than the tax rate that…

Reducing Risk With a Diversified Portfolio

Reducing Risk With a Diversified Portfolio Have you been worried about the stock market’s recent volatility? You’re not alone. The stock market in March was a roller-coaster ride that served as a reminder to investors that the market’s ups and downs can be a little dizzying. But a volatile market should not leave you feeling…

Are You Defining Items in QuickBooks Correctly?

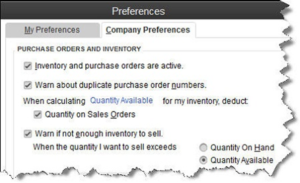

[vc_row][vc_column][vc_column_text] Create item records in QuickBooks carefully, and QuickBooks will return the favor by running useful, accurate reports. Figure 1: Clearly-defined items result in precise reports. Obviously, you’re using QuickBooks because you buy and/or sell products and/or services. You want to know at least weekly — if not daily — what’s selling and what’s…

Saving Money for College: Education Credits

Saving Money for College: Education Credits Education credits are tax credits available for qualified education expenses paid by the taxpayer in the furthering of their education. Qualified education expenses are defined as an expense paid during the tax year for tuition and fees required by an eligible educational institution for student enrollment and attendance. Room…