Sales Tax Deduction Option, State and Local

[vc_row][vc_column][vc_column_text]

Sales Tax Deduction Option, State and Local

The Tax Relief and Health Care Act of 2006 extended the election to deduct state and local general sales taxes for 2006. The act was enacted after Schedule A (Form 1040), Itemized Deductions, and its instructions were printed. Because we were not able to include the instructions for figuring the deduction in the Schedule A instructions, we are providing this publication to help you figure this deduction.

You can elect to deduct state and local general sales taxes instead of state and local income taxes as a deduction on Schedule A. You cannot deduct both. To figure your deduction, you can use either:

- Your actual expenses, or

- The optional sales tax tables plus the general sales taxes paid on certain specified items.

IRS Publication 600, Optional State Sales Tax Tables, helps taxpayers determine their sales tax deduction amount in lieu of saving their receipts throughout the year. Taxpayers use their income level and number of exemptions to find the sales tax amount for their state. The table instructions explain how to add an amount for local sales taxes if appropriate.

Taxpayers also may add to the table amount any sales taxes paid on:

- A motor vehicle, but only up to the amount of tax paid at the general sales tax rate; and

- An aircraft, boat, home (including mobile or prefabricated), or home building materials, if the tax rate is the same as the general sales tax rate.

For example, the State of Washington has a motor vehicle sales tax of 0.3 percent in addition to the state and local sales tax. A Washington state resident who purchased a new car could add the tax paid at the general sales tax rate to the table amount, but not the 0.3 percent motor vehicle sales tax paid.

Taxpayers will claim the deduction on line 5 of Schedule A, checking a box to indicate whether the amount represents sales tax or income tax.

While this deduction will mainly benefit taxpayers with a state or local sales tax but no income tax — in Alaska, Florida, Nevada, South Dakota, Texas, Washington and Wyoming — it may give a larger deduction to any taxpayer who paid more in sales taxes than income taxes. For example, you may have bought a new car, boosting your sales tax total, or claimed tax credits, lowering your state income tax.[/vc_column_text][/vc_column][/vc_row]

How to Successfully Sell Your Company

How to Successfully Sell Your Company Tips for Privately-Held Business Owners By Jason Pfannenstiel Be clear about your motivation for selling. Reason for the sale is among the first questions buyers will ask. Your personal and professional reasons should be more than simply wanting to cash out for a certain magical dollar value. Before you…

15 Ways to Improve Your Cash Flow Now

15 Ways to Improve Your Cash Flow Now By Howard Fletcher Cash management theory and techniques are well understood and practiced by treasury managers in large corporations. They use sophisticated models and cash management tools that allow them to predict and manage cash. Many of these are beyond the reach or need of small companies.…

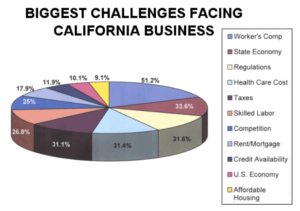

Survey: Biggest Challenges Facing California Businesses

Survey: Biggest Challenges Facing California Businesses A recent survey was conducted to determine what business owners in California thought the biggest challenges facing their businesses were. Out of 1500 questionnaires, these are the percentage of respondents who checked off a box next to each challenge. (Respondents were allowed to select more than one box, so…

5 Strategies to Successful Cash Flow Management

5 Strategies to Successful Cash Flow Management By John Reddish How can you predict, avoid and/or, minimize the impact of a cash emergency? Managing cash flow is every manager’s challenge, every day, every year. Those managers who keep a close eye on their daily activity and emerging industry trends can help reduce their company’s exposure…