Startups Should Pay Heed to These Tax Tips

Tax season us winding down and there’s a good chance that most businesses have already filed their tax returns. If you’re a business owner and you still haven’t filed then contact us right away to get it done. In any case, now is a good time to review some tax tips for businesses, especially for those companies that are just starting out. As a startup you have to be sure you’re doing everything you can to help minimize your taxes and maximize your revenue.

One mistake some owners of startup companies make is to overlook their accounting and taxes because they’re so focused on growing their business and improving their bottom line. However, this can be very costly. After all, a lower tax bill means a greater bottom line. So what should startups be looking for when it comes to their taxes?

- Keep The Books – any business, including a startup, needs to have a good bookkeeping system set up right from the get-go. Don’t wait till “some other day” to keep a detailed record. Start from the beginning and never get behind.

- Hire a CPA – finding a good certified public accountant (CPA) is a very smart move. The right CPA can get you pointed in the right direction right off the bat. He or she can also help you choose the right bookkeeping software for you business and show you how to set yourself up for the best tax results.

- Keep Business & Personal Separate – make sure you always keep your business and personal purchases separate. Get a card for business and use it for business expenses.

- Retirement Plan – if you can afford it, set up a retirement plan for your employees. It’s an attractive incentive and it gives you another tax break.

- Estimated Taxes – make sure you are paying sufficient estimated taxes throughout the year.

These are some smart moves to make for any business, whether you’re just starting out or not. If you need sound accounting advice or tax information regarding your business, then please contact GROCO today at 1-877-CPA-2006, or click here.

Reducing Risk With a Diversified Portfolio

Reducing Risk With a Diversified Portfolio Have you been worried about the stock market’s recent volatility? You’re not alone. The stock market in March was a roller-coaster ride that served as a reminder to investors that the market’s ups and downs can be a little dizzying. But a volatile market should not leave you feeling…

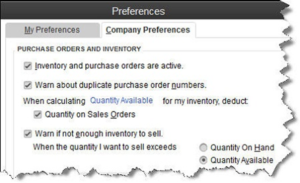

Are You Defining Items in QuickBooks Correctly?

[vc_row][vc_column][vc_column_text] Create item records in QuickBooks carefully, and QuickBooks will return the favor by running useful, accurate reports. Figure 1: Clearly-defined items result in precise reports. Obviously, you’re using QuickBooks because you buy and/or sell products and/or services. You want to know at least weekly — if not daily — what’s selling and what’s…

Saving Money for College: Education Credits

Saving Money for College: Education Credits Education credits are tax credits available for qualified education expenses paid by the taxpayer in the furthering of their education. Qualified education expenses are defined as an expense paid during the tax year for tuition and fees required by an eligible educational institution for student enrollment and attendance. Room…

Thinking About Giving up Your U.S. Citizenship? Think Twice

Thinking About Giving up Your U.S. Citizenship? Think Twice While not a lot of people ever entertain the thought of giving up their U.S. citizenship, there are more people every year that are making that choice. Among them are several wealthier people whose main reason for renouncing is to escape the country’s overloaded tax system;…