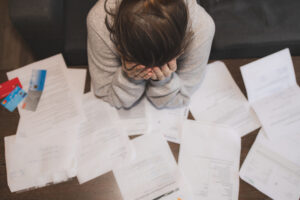

What Do You Do When You Owe Taxes But Don’t Have the Funds?

For many people tax season brings the joy of a nice big refund to go out and splurge on something they’ve had your eye on for a long time. On the flip side of the equation are those people who surprisingly, or not, end up owing the IRS money. Not only do these people miss out on the extra cash influx, but they also have to come up with the funds to pay off the extra tax bill.

For some people, depending how high the bill is, they could have to pay even more than just the shortage amount. That’s because many times when people underpay they end up owing penalties for the underpayment. For those who owe a lot of money, those penalties could end up being huge. In fact, the penalties can even be much higher than the shortage.

That’s why it’s always best to try to avoid owing any money to the IRS, especially if you don’t have the funds to pay it off when the tax bill comes due. So what happens to people who can’t pay their tax bill? You do have a few options.

In some cases, it might be a good idea to take out a loan or a line of credit in order to pay off the bill. Of course, you will then be responsible to pay off the loan, so use caution. Another option is to apply for an extension with the IRS. This could buy you a little time to come up with the needed funds. If you need even more time then try applying for a hardship extension, which could give you up to six months to pay it off. You could also ask the IRS for permission to set up a payment plan to pay off the debt in installments.

Whichever path you decide to take, make sure you do something. Don’t ignore the problem or it will only get worse. The penalties will likely increase the longer you wait and the IRS could eventually take other measures or even press charges. So the bottom line is: do something.

Making Your Medical Deductions Count

Making Your Medical Deductions Count April 15th is almost here and if you are owing tax it may pay to take a second look at that return to see if you claimed all medical deductions you are entitled to. Your diligence in keeping track of expenses will pay off. IRS Publication 502 has a complete listing…

GROCO Warns of Common Tax Filing Mistakes

GROCO Warns of Common Tax Filing Mistakes Tax return anxiety is on the rise as the federal tax filing date looms. The prospect of filing an erroneous return increases as more rely on tax software to help prepare their returns. For the week ending March 28, more than 10,000 electronic returns were filed from home…

Loss on Sale of 1244 Stock

Have you considered a loss on sale of 1244 stock as a tax strategy? Ordinarily, a loss on a sale or exchange of stock is a capital loss. Capital loss treatment is generally less advantageous than ordinary deduction treatment because of the fact that a capital loss recognized by an individual is applied, first against…

Section 213 Medical, Dental, etc., Expenses

Section 213 Medical, Dental, etc., Expenses (a) Allowance of deduction There shall be allowed as a deduction the expenses paid during the taxable year, not compensated for by insurance or otherwise, for medical care of the taxpayer, his spouse, or a dependent, to the extent that such expenses exceed 7.5 percent of adjusted gross income.…