Things to Consider for Your 2015 Capital Gains Tax

There are all kinds of investors in the world. Some are looking to make a quick buck by buying and then quickly selling stocks as soon as they increase in value. Other investors buy stocks with an eye toward the future, which means they are in it for the long haul.

In any case, anyone who invests wants to be successful at it. It’s a great feeling to buy stock in a company and see that stock increase in value. However, at some point if you plan on selling that stock and cashing in or your gains, you will have to give a portion of those gains to the taxman. What percentage you will owe will depend on the size of your gain and how long you have owned the stock.

The government wants investors to hold onto their stocks longer. To encourage this they have a lower tax percentage on stocks held longer than a year. Whether you’re a quick turnaround trader or a long-term investor here’s what you should be aware of in 2015 for your capital gains taxes.

First, generally all you need to know to determine your capital gains is the difference between what you paid for the stock and how much you sold it for. When you know that amount then you can calculate the tax. Your tax rate will depend on which bracket you’re in. There are three that apply:

- If your ordinary income puts you in the 10-15 percent tax bracket, then your long-term capital gains rate is 0 percent.

- If your ordinary income falls in one of the 25, 28, 33, or 35 percent tax brackets then your long-term capital gains rate is 15 percent.

- If your ordinary income is in the 39.6% tax bracket, then your long-term capital gains rate is 20%.

There are a few other caveats to remember. For high-income earners, there is an additional 3.8 percent surtax on net investment income. Also, you only pay taxes on the net of your capital gains, which can make a big difference if you sell more than one stock in a year. If you want to learn more about capital gains taxes then please contact GROCO for more answers. Click here or call us at 1-877-CPA-2006.

Making Tax-wise Investments

Making Tax-wise Investments Tax considerations are not, and should never be, the be-all and end-all of investment decisions. The choice of assets in which to invest, and the way in which you apportion your portfolio among them, almost certainly will prove to be far more important to your ultimate results than the tax rate that…

Reducing Risk With a Diversified Portfolio

Reducing Risk With a Diversified Portfolio Have you been worried about the stock market’s recent volatility? You’re not alone. The stock market in March was a roller-coaster ride that served as a reminder to investors that the market’s ups and downs can be a little dizzying. But a volatile market should not leave you feeling…

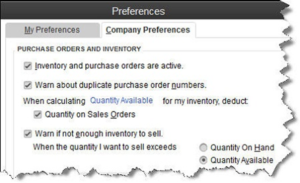

Are You Defining Items in QuickBooks Correctly?

[vc_row][vc_column][vc_column_text] Create item records in QuickBooks carefully, and QuickBooks will return the favor by running useful, accurate reports. Figure 1: Clearly-defined items result in precise reports. Obviously, you’re using QuickBooks because you buy and/or sell products and/or services. You want to know at least weekly — if not daily — what’s selling and what’s…

Saving Money for College: Education Credits

Saving Money for College: Education Credits Education credits are tax credits available for qualified education expenses paid by the taxpayer in the furthering of their education. Qualified education expenses are defined as an expense paid during the tax year for tuition and fees required by an eligible educational institution for student enrollment and attendance. Room…